Personal service tax certificate

A1 proofreading not yet effective for this page. In the meantime, you can ask any questions on the forum.

A1 proofreading not yet effective for this page. In the meantime, you can ask any questions on the forum.

In France, companies in the personal services sector issue an annual tax certificate, which allows their clients to recover part of the sums paid, in the form of an income tax credit equal to 50% of expenses and in the limit of a ceiling.

The French civil service does not appreciate things being too simple, so “minor” complications have been added. Thus, in 2018, the maximum ceiling is 12,000 euros, adjustable depending on the number of children and ascendants, the disabled counting for more, but with a limit of 5,000 euros for gardening, 3,000 for IT assistance, and 500 for DIY, knowing that an intervention should not take 2 hours, and the washing of tiles limited to a third of the total glazed surface per period of 4 consecutive months without rain, or 2 months with rain*.

It should be noted that it is up to the beneficiary to verify these thresholds, and to declare the correct amounts in the correct boxes. Fortunately, you can edit this certificate for your customers, via Gestan.

* no, for this last activity, it was a joke, but admit that you believed it!

Using the screen

The prerequisite for publishing tax certificates is a three-step process for monitoring interventions:

- recording of interventions carried out via the intervention management screens

- invoicing of interventions

- collection of payments

Via the right click on the intervention list screen, request the edition of the INT3 state. You can request it for a customer, or for all customers, for a date range (normally the fiscal year).

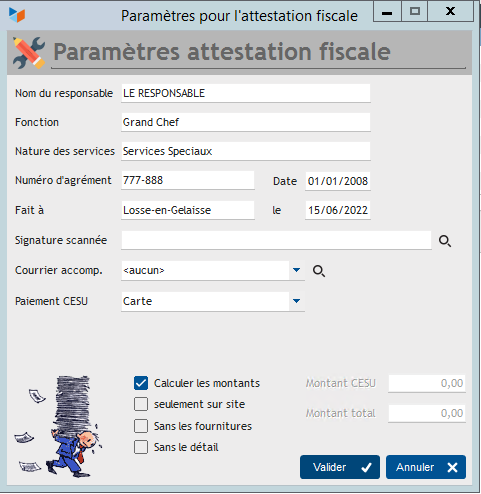

The screen that then opens allows you to enter the parameters necessary for the tax certificate.

You must provide the Name of the manager and his function, the nature of the services, the approval number and the approval date of the company for the personal service activity.

Below, also provide the place (made at) and the date the certificate was issued. It is possible to sign the certificates manually, or to use a scanned signature. It is also possible to edit an accompanying letter.

The calculation of the amounts paid differentiates the amounts paid in CESU (Chèque Emploi Service Universel, a payment method used in France) from other payment methods, which is why it is necessary to specify which of the payment methods you have configured which represent a CESU payment (call it CESU in the payment method settings).

The Calculate amounts box allows you to calculate, or not, the amounts paid by the customer. They are calculated on the basis of entries recorded in payment of invoices issued within the specified date range. In case you request the certificate for a single customer, you can force amounts to any value of your choice.

The box Only on site allows only interventions that were carried out on the customer's site to be taken into account.

The box Without supplies allows, in the case where you have requested the calculation of totals, to exclude from them any invoice line for a product attached to a “supply” type family (supplies do not would not give rise to tax relief…) If a product line does not have a product code, or if this product is not found in the product table (case of non-catalogue products), it is considered by default as “supply”, so the product line is excluded from the total.

You can also publish, or not, the list of interventions. This is what the Without detail box is for.

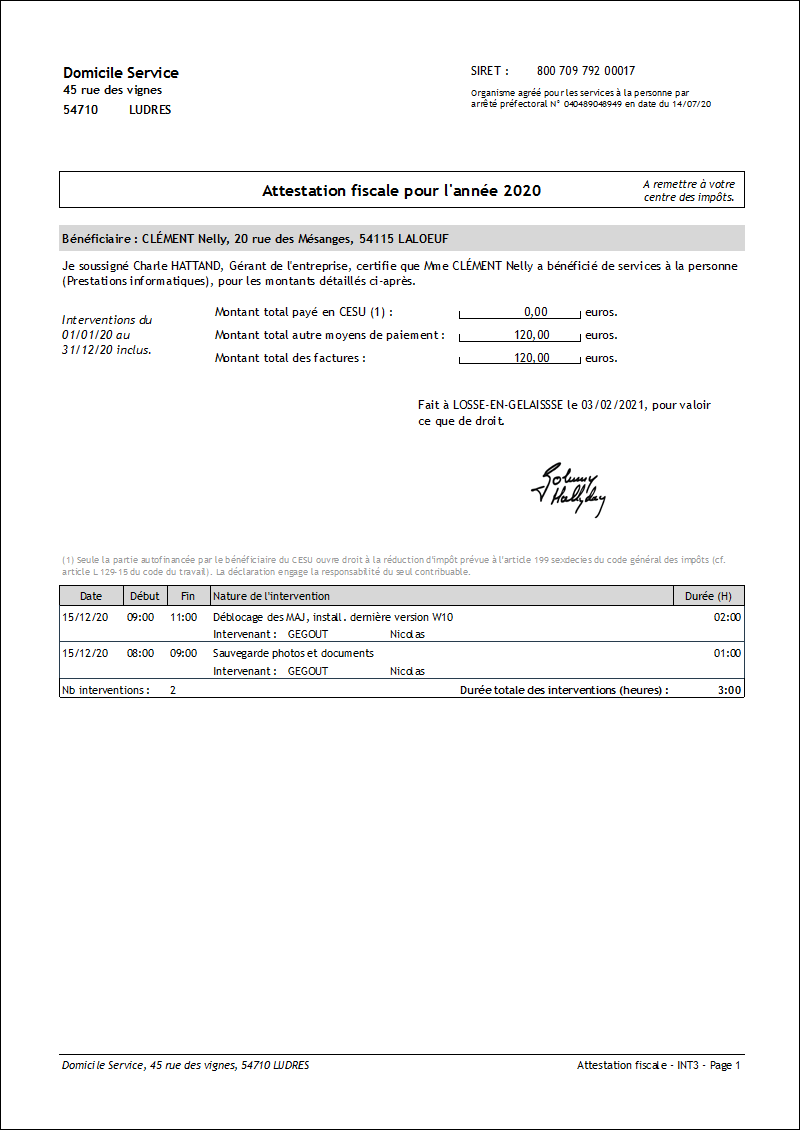

Below is an example of a personal service tax certificate.

Details of the calculation of the amounts

These certificates are issued on the basis of recorded collection entries (payments actually made). An invoice issued on December 31, but for which payment would be made on January 5 of the following year, would therefore not be taken into account in year N, but in the year of payment, in this case N+1 .

Reference texts

All personal service organizations must communicate before March 31 of year N+1 to each of their clients an annual tax certificate, in order to allow them to benefit from the tax advantage (tax credit) under of year N.

This certificate must mention:

- the name and address of the intervening organization,

- the number and date of registration of the declaration,

- the name and address of the person who benefited from the service and, if applicable, the number of their debited account,

- a summary of the interventions carried out (name and identification number of the participants, dates and duration of the interventions). For the sake of simplification, if the services were carried out every day or periodically, a monthly grouping of interventions could be established,

- the amount actually paid.

In cases where services are paid in pre-financed CESUs, the certificate must indicate to the client that he is required to clearly identify to the tax services, during his annual tax declaration, the amount of CESUs he is paying. personally financed, this amount alone giving rise to a tax advantage.

This clarification will be made possible in particular thanks to the issuance, by the legal entities which pre-finance the CESU (employers, pension funds, mutual societies, etc.), of an annual certificate to the beneficiary establishing the number, amount and pre-financed share of the Cesu which were attributed to him.

See also http://www.servicesalapersonne.gouv.fr

Other Activity articles

Other Activity articles

On the same theme: AICI Extension (Immediate Advance Tax Credit) URSSAF